On a humid afternoon in a tier-3 town, a tour operator laid out a practical business plan before Piramal Finance’s research team. Running a small fleet of Maruti Swift Dzires, he hoped to upgrade to seven-seater Maruti Ertigas. His four-tonne commercial vehicles were also due for sturdier replacements.

His ambition was straightforward: to expand without bending the rules. If caught violating regulations, he told the Piramal Finance team, authorities could seize his vehicles. That risk alone made him choose thin margins over shortcuts.

The one thing missing was capital. The willingness to adopt formal credit came with anxiety about how to access it.

For Piramal Finance, this was a familiar pattern. Across semi-urban India, small entrepreneurs and salaried households weren’t short on ambition; they were short on lenders willing to understand their daily realities.

“How we operate is that we underwrite using data, the physical nature of their work, having personal discussions with them at their workplace, then go from there,” said Arvind Iyer, Piramal Finance’s chief marketing officer.

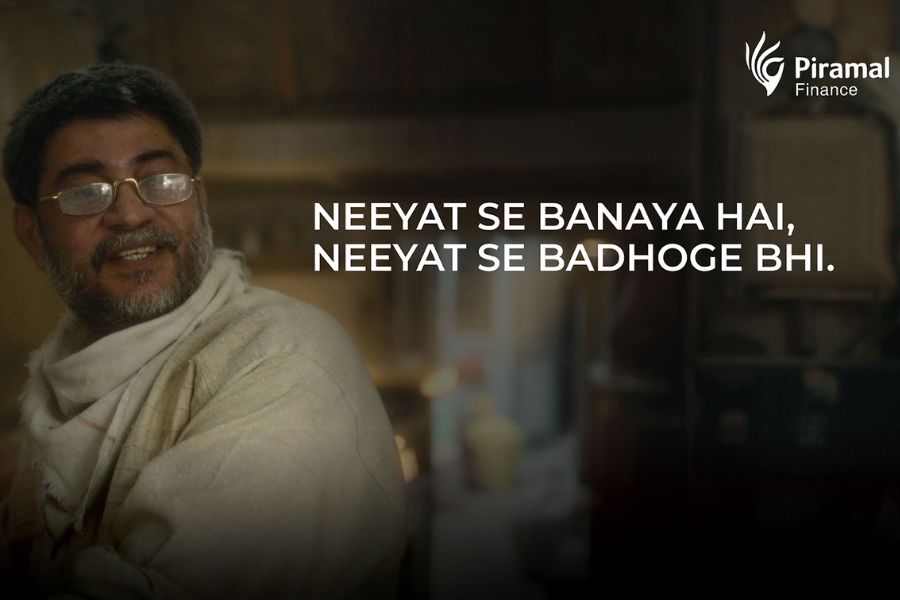

This combination of data paired with lived context has shaped the financial services company’s brand proposition, Neeyat (Intent), now in its third chapter.

Turning lived insight into brand narrative

Launched four years ago alongside the company’s retail finance business, Neeyat was designed to make customers feel seen. “When we started out as a retail finance business four years ago, and when we launched Neeyat, we wanted to portray to our customers that somebody is looking at them,” Iyer said.

Early campaigns captured the small but consequential choices of self-employed workers and salaried earners. Over time, as Piramal Finance’s teams travelled through Karnataka, Telangana, Tamil Nadu, NCR, and Maharashtra, conducting regular ethnographic research, the stories evolved.

“One thing that kept coming back was their aspiration and growth quotient,” Iyer said. Semi-urban borrowers were no longer stuck at the entry gate of the credit ecosystem; many had already moved a step or two forward. Incomes among customers in these markets had increased, with median household incomes rising by 1.5x. Many customers weren’t new to credit; they now sought higher ticket loans or asset upgrades.

These insights informed Neeyat 3.0. The latest edition focuses not on those seeking their first loan, but on people who already know what they want and how they intend to progress, provided a lender recognises their intent and not merely their paperwork. “That’s the blueprint of how we constructed this year's campaign proposition,” Iyer said.

Real India, not its studio version

The new campaign features three films rooted in specific regional contexts rather than generic small-town imagery. “Like the ‘Chakki’ is a northern phenomenon. Then the ‘Bakery’ comes from Telangana or the 'Istri' one, which has a very northern tonality,” said Iyer.

Avoiding glossy recreations, the team insisted on authenticity in location, nuance and character detailing. “We took it upon ourselves to be authentic in the portrayal of our real customer. The locations aren’t sets, but resemble what such places would be in real life,” the brand marketer said.

Budget limitations forced selective choices instead of broad representation across states. But the chosen markets were ones where dialect, body language and behavioural cues could anchor each narrative naturally.

Research formed the backbone of this creative approach. Iyer’s team conducted interviews across five major markets with customers and channel partners, bringing back clips and pen-portraits. These became reference points for the campaign’s directors. “While they have creative liberties cinematically, they can tie it to our research findings and it has an authentic representation of India,” Iyer said.

The result stands in contrast to an industry where financial advertising often defaults to sleek urban offices and generic aspirational tropes.

Translating creative work to business metrics

Piramal Finance positions Neeyat not as brand advertising but as an acquisition engine. Early numbers from previous editions underscore that claim.

Iyer claimed that the debut put the company on the map with its distributor network, employees and existing customers and also nudged partner confidence in smaller cities. Brand salience rose 2.5x, while consideration nearly tripled due to ATL, BTL and digital exposure.

The campaign reached over 2.5 lakh consumers; a little over 30% were sanctioned loans. Ticket sizes improved by nearly 500 basis points, which is meaningful for a new retail-lending entrant.

Neeyat 2.0 sharpened the funnel. Incoming customers already had credit histories and were looking to upgrade. “Hence, our ticket sizes went up and we even saw that the kind of credit profile coming through the door started to improve,” Iyer said.

Secured products, which are typically harder and slower to convert, rose sharply, with sanctions increasing over 50%.

The impact often extended beyond the formal campaign window. Customers approached the company through call centres, branches and website forms long after ads stopped running. This cumulative effect continues to shape Piramal Finance’s efforts to improve turnaround time and customer journeys.

With Neeyat now in its third year, the natural question is whether the storytelling arc risks fatigue. Iyer is cautious. “Let’s wait and watch to have a conversation in a few months to see the numbers before coming to a conclusion.” He believes Neeyat works because it reflects the firm’s operational philosophy, as the product is the brand proposition in many ways.

Distribution backs the story

A lending brand’s real distribution lies not in campaigns but in its channel network. India’s credit ecosystem depends heavily on direct sales agents (DSAs), local connectors and micro-intermediaries who steer customers through paperwork, product discovery, and lender selection.

Since Neeyat 1.0, Piramal Finance’s partner base has expanded dramatically. “We had around 4000–5000 channel partners; today, we have over 15,000 to 20,000 connectors and an over-10,000 DSA network pan-India in around 517 branches,” Iyer said.

DSAs run neighbourhood shops; connectors operate informally on their phones, recommending lenders based on hyperlocal experience. For both groups, campaigns serve as conversation starters and validation tools. Calls-to-action in every film route customers towards these sales channels.

Internal partner tracking shows a clear shift. Preference for Piramal Finance among partners has increased about 1.5 times since the first campaign. Enthusiasm on the ground is another sign. “Some channel partners tend to give great feedback asking if we can give them shorter edits, or give me options for their WhatsApp DP,” Iyer said.

The firm monitors reactions across its 500-plus branches through townhalls and qualitative assessments. This network—more than 30,000 frontline staff and thousands of partners—forms the operational scaffolding behind the Neeyat narrative.

Despite the growing importance of digital, offline remains central. “We don't rely only on when the campaign comes up to be on-ground, but are on-ground throughout the entire year across our 500+ branches,” Iyer said. The focus now is strengthening DNA markets; the regions where brand strength lags the national average. Local events, festival integrations, partner meets and even street plays remain part of the mix.

Piramal Finance works with independent agency The Womb. Both teams conduct ethnography together. On choosing an independent shop, Iyer said, “I attribute a lot to being at the right place at the right time, and the quality of the conversation you land up having, and within that, figuring the chemistry.” His longstanding relationship with co-founders Kawal Shoor and Navin Talreja played a role. “It has been a great partnership with them.”

A brand at an inflection point

The Neeyat franchise is an unusual case in Indian financial marketing: a young lender betting on slow, culturally grounded storytelling in a sector dominated by transactional pitches. Its success so far rests on a simple principle, where it borrows authenticity from the field rather than manufacture it in studios.

But as India’s credit-seeking middle expands and competition intensifies, Piramal Finance will need to sharpen the next chapters. The challenge is maintaining cultural specificity without narrowing appeal, and scaling distribution while staying close to the ethnographic roots that fuel the brand.

Iyer remains pragmatic. “We're fairly data-driven. We’ll put that in, and then we’ll figure getting the anecdotal commentary when we visit markets… It’s a conversation we can have in a few months.”

For now, Neeyat sits at a crossroads. Armed with data, grounded in lived reality, it is trying to write real Indian ambition into its marketing, one customer story at a time.