Please sign in or register

Existing users sign in here

Having trouble signing in?

Contact Customer Support at

[email protected]

or call+91 22 69489600

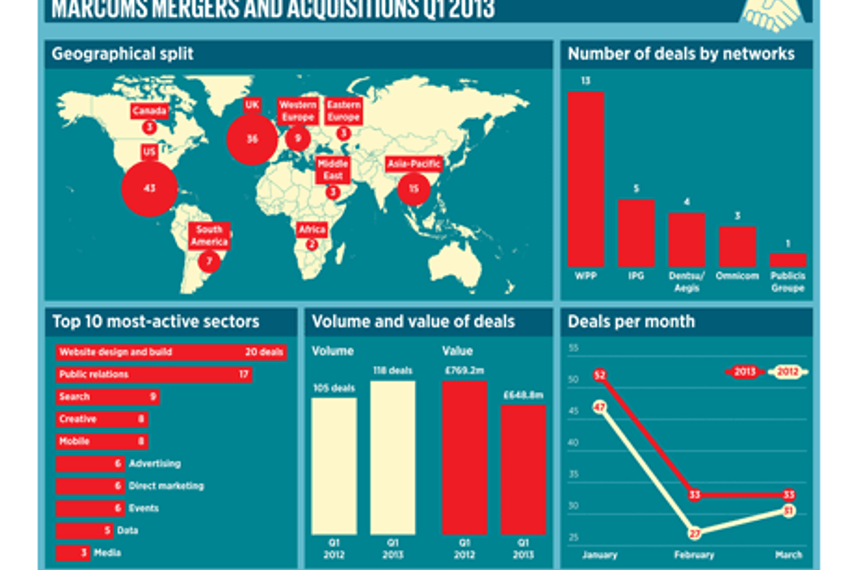

Mergers and acquisitions are changing as networks look to new technology and emerging markets.

Contact Customer Support at

[email protected]

or call+91 22 69489600

Top news, insights and analysis every weekday

Sign up for Campaign Bulletins

.jpg&h=268&w=401&q=100&v=20250320&c=1)

Following an operational disruption earlier this year, the renewed brand direction focuses on resilience, intent and community connection.

.jpg&h=268&w=401&q=100&v=20250320&c=1)

IAA India and Snapchat brought together agencies and creators for a hands-on look at AR’s growing role.

Here's something that might surprise media planners: when someone watches live sports on their TV, and someone else watches on their phone, they're probably not the same person switching devices. They're actually different audiences.

.jpg&h=268&w=401&q=100&v=20250320&c=1)

Amazon Prime Video and WPP OpenDoor executed a multi-platform rollout for The Family Man Season 3, integrating the series into everyday viewer environments.

.jpg&h=334&w=500&q=100&v=20250320&c=1)

.jpg&h=334&w=500&q=100&v=20250320&c=1)

.jpg&h=334&w=500&q=100&v=20250320&c=1)

.jpg&h=334&w=500&q=100&v=20250320&c=1)