Please sign in or register

Existing users sign in here

Having trouble signing in?

Contact Customer Support at

[email protected]

or call+91 22 69489600

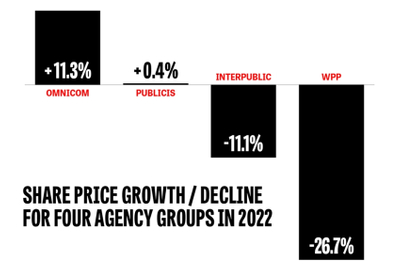

The study finds a greater array of both buyers and sellers in marketing and communications

Contact Customer Support at

[email protected]

or call+91 22 69489600

Top news, insights and analysis every weekday

Sign up for Campaign Bulletins

AMD’s Zen Mode film imagines an office where pressure disappears by using calm, not jargon, to make enterprise tech feel human.

The martech agency is executing a 26-company acquisition roadmap to achieve a 100-crore profit benchmark for its public market debut.

.jpg&h=268&w=401&q=100&v=20250320&c=1)

The wedding-focused campaign combines celebrity association, consumer contests and in-store activations to engage shoppers during the festive marriage season.

.jpg&h=268&w=401&q=100&v=20250320&c=1)

The digital-first campaign with Sahher Bambba highlights easy-to-use styling tools designed for quick salon-like results.