Please sign in or register

Existing users sign in here

Having trouble signing in?

Contact Customer Support at

[email protected]

or call+91 22 69489600

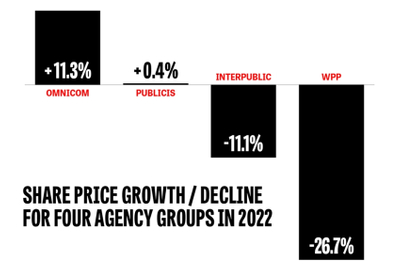

Private equity has been looking at agency groups

Contact Customer Support at

[email protected]

or call+91 22 69489600

Top news, insights and analysis every weekday

Sign up for Campaign Bulletins

.png&h=268&w=401&q=100&v=20250320&c=1)

Between comparison charts and keywords searches, the humble product page has begun to lose its shine.

.png&h=268&w=401&q=100&v=20250320&c=1)

The era of the accountable, standardised ecosystem is beginning.

.png&h=268&w=401&q=100&v=20250320&c=1)

From global awards to brave work, Indian independent ad agencies are grateful that for the opportunity to come out of the shadows of larging holding companies.

.png&h=268&w=401&q=100&v=20250320&c=1)

What we call 'media fragmentation' is simply reality catching up with an industry that prefers linear planning templates.